Understanding Inflation and Economic Volatility: How It Impacts Your Investments

Investing during inflation and economic volatility requires a clear understanding of what these terms mean and how they affect your financial future. Inflation is the rise in the general price level of goods and services over time, which reduces the purchasing power of your money. When inflation is high, the same amount of money buys fewer goods, making it crucial to ensure your investments grow at a pace that outpaces inflation. Economic volatility, on the other hand, refers to unpredictable fluctuations in financial markets, interest rates, and the overall economy, often caused by global crises, political instability, or sudden changes in consumer behavior.

During periods of high inflation or volatile markets, traditional savings accounts and low-yield investments often fail to preserve wealth. For example, keeping money in a bank account that offers 3% annual interest when inflation is 7% effectively reduces your money’s value. Similarly, stocks or bonds can experience sudden drops in value during market turbulence, making it critical for investors to adopt strategies that protect their assets and maintain growth potential.

Understanding the dynamics of inflation and market volatility empowers investors to make informed decisions, minimize risks, and take advantage of opportunities that arise even in uncertain economic times. Recognizing these forces is the first step toward crafting a resilient investment plan that withstands financial turbulence and safeguards long-term wealth.

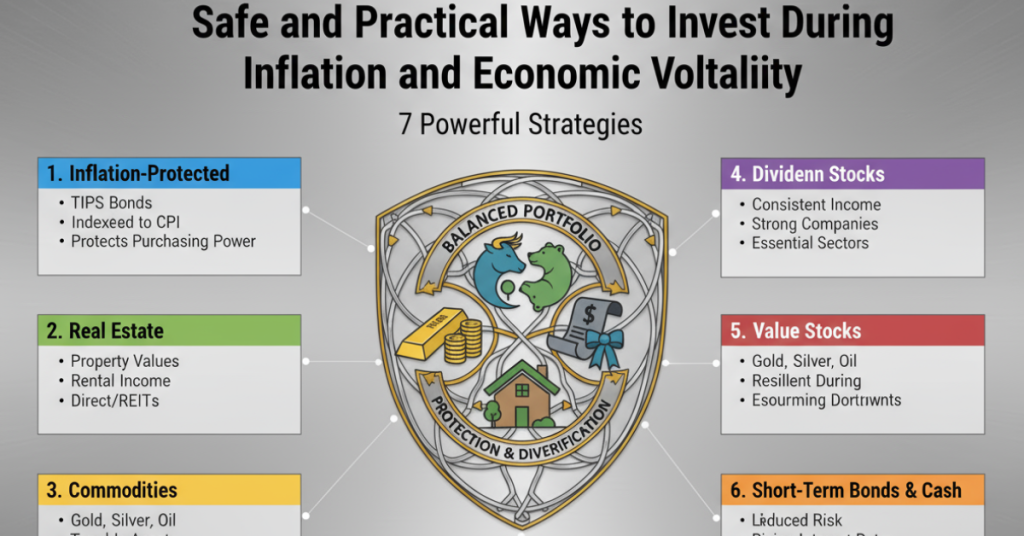

7 Powerful Investment Strategies to Protect Your Wealth

During inflation and economic volatility, smart investors focus on strategies that not only preserve capital but also generate steady returns. Below are seven practical and proven investment approaches that can help protect your money while maintaining growth potential in uncertain times.

1. Invest in Treasury Securities

Government-backed Treasury bills and bonds are among the safest investments during inflation. These securities are guaranteed by the government and provide predictable returns. Inflation-protected securities such as Treasury Inflation-Protected Securities (TIPS) adjust their value with inflation, ensuring your purchasing power is maintained. For investors seeking stability and minimal risk, this is a reliable option.

Learn more from the official U.S. Treasury resource.

2. Real Estate as a Hedge Against Inflation

Real estate tends to appreciate in value as prices rise, making it a natural hedge against inflation. Rental properties generate passive income, and real estate investment trusts (REITs) allow investors to gain exposure without directly owning property. During inflationary periods, landlords can often increase rent, which offsetss higher living costs. For Nigerians, investing in local housing developments or commercial spaces can offer similar protection.

Companies that pay consistent dividends often perform better during economic uncertainty because they provide regular income even when market prices fluctuate. Focus on firms with strong balance sheets and a history of increasing dividends over time, such as those in utilities or consumer staples. Reinvesting dividends can compound your returns and build long-term wealth.

4. Gold and Precious Metals

Gold has long been seen as a safe-haven asset. When currencies lose value due to inflation, gold often rises in price. It’s not just gold — silver and platinum can also serve as stores of value. You can invest directly in physical metals or through exchange-traded funds (ETFs) that track their performance. Although gold prices can fluctuate, they tend to hold value better than fiat currencies during turbulent times.

5. Commodities and Energy Investments

Commodities such as oil, natural gas, and agricultural products often increase in value when inflation rises. Investing in commodity-focused funds or energy companies can help balance your portfolio. These assets provide a buffer since rising commodity prices usually drive inflation itself, offering a natural hedge for investors.

External Link Suggestion: Explore global commodity market trends (Visit our in-depth post on profitable commodity investing).

6. Inflation-Protected Bonds

In addition to Treasury securities, many countries issue inflation-indexed bonds. These bonds increase their principal and interest payments in line with inflation rates. They’re ideal for investors looking for low-risk options that preserve real value. For example, Nigeria’s inflation-linked savings bonds allow local investors to protect purchasing power even in unstable times.

External Link Suggestion: Visit our full guide on inflation-linked bonds and how they secure real returns.

7. Diversified Exchange-Traded Funds (ETFs)

ETFs offer exposure to a wide range of assets — stocks, commodities, and bonds — through a single investment. A diversified ETF can balance risk while maintaining growth potential. Choosing ETFs that focus on defensive sectors or global diversification helps reduce volatility and stabilize returns. For example, combining U.S., African, and Asian ETFs gives investors a broader safety net against local economic shocks.

By adopting these seven strategies, investors can safeguard their wealth and maintain consistent growth even in uncertain times. The key is to balance risk with opportunity and ensure every investment choice contributes to long-term financial resilience.

![]()

Building a Resilient Investment Portfolio During Economic Uncertainty

A resilient investment portfolio is your shield against inflation and market volatility. The goal is not just to survive uncertain times but to thrive through smart diversification, informed decisions, and disciplined financial planning. When markets fluctuate and currencies lose value, having a portfolio that adapts to changing conditions ensures stability, growth, and peace of mind.

The first step to building resilience is diversification — spreading your investments across multiple asset classes such as stocks, real estate, bonds, and commodities. Diversification minimizes the impact of a downturn in any single market and allows gains in one sector to offset losses in another. For instance, if stock prices decline during inflation, real estate or gold may appreciate, balancing your overall returns.

Next, focus on risk management. Investors often make the mistake of reacting emotionally to economic turbulence, which leads to poor decisions. Setting clear risk tolerance levels helps you stay focused on long-term objectives. Avoid placing all your funds in volatile assets; instead, mix low-risk investments like Treasury securities with growth-oriented assets like dividend-paying stocks or ETFs. This approach balances safety and performance even when the market shifts rapidly.

Regular portfolio reviews are equally important. Inflation rates, interest policies, and market conditions can change within months. Rebalancing your portfolio quarterly or annually ensures that your investments remain aligned with your goals and risk appetite. You might need to reduce exposure to certain assets and increase others as economic indicators evolve. Tools like portfolio trackers and investment apps can simplify this process and help monitor performance effectively.

Another vital component is maintaining liquidity. During economic instability, having access to cash or liquid assets allows you to seize opportunities, such as buying undervalued stocks or property. It also provides a financial cushion in case of emergencies, preventing you from selling long-term assets at unfavorable prices.

Finally, cultivate a mindset of long-term investing and patience. Historically, markets recover from downturns and reward those who stay invested. As global economies stabilize, assets that were undervalued during inflationary periods often yield strong returns. Working with certified financial advisors can also provide tailored guidance and reduce emotional decision-making.

External Link Suggestion: For practical portfolio balancing tips, read our comprehensive guide on creating a diversified investment plan (Visit our full guide on building a balanced investment portfolio).

A resilient portfolio doesn’t rely on luck but on strategy, balance, and informed choices. By applying the seven investment strategies discussed earlier within a diversified, well-reviewed portfolio, you position yourself for stability and growth even when inflation and volatility dominate the global economy.

FAQ Section

1. What is the safest investment during high inflation?

The safest investments during high inflation are Treasury Inflation-Protected Securities (TIPS), real estate, and gold. These assets retain value and adjust with inflation, offering protection against purchasing power loss.

2. How often should I rebalance my investment portfolio?

Ideally, review your portfolio every three to six months or when major economic changes occur. Rebalancing ensures your investments remain aligned with your financial goals and risk tolerance.

3. Should I hold cash during economic volatility?

Holding some cash is wise for liquidity and quick opportunities, but excessive cash loses value during inflation. Keep a balance between liquid assets and growth investments.

4. Can investing during inflation still be profitable?

Yes. Investors who diversify across inflation-protected assets, commodities, dividend stocks, and real estate often achieve steady growth despite inflationary pressures.

5. Is real estate still a good investment when interest rates rise?

While rising rates can affect affordability, real estate remains a strong hedge against inflation because property values and rental income often increase with overall price levels.

For more useful insights like this, visit our complete resource page on Personal Development, where we cover strategies, tips, and recommendations designed to help you grow.